It’s not a cheese, wine, or bath products advent calendar…but beginning December 1 through Christmas Day the GoFisch blog will feature a new piece related to giving. ‘Tis the season for giving and the “25 Days” posts will feature information important for both nonprofit executives and donors.

https://www.gordonfischerlawfirm.com/wp-content/uploads/2017/11/Copy-of-Christmas-Icons-Funny-Card.png315828Gordon Fischerhttps://www.gordonfischerlawfirm.com/wp-content/uploads/2017/05/GFLF-logo-300x141.pngGordon Fischer2019-11-30 20:18:432020-05-18 11:28:4125 Days of Giving Starts December 1

I would like to wish you a very happy Thanksgiving. I hope that you have the opportunity to spend quality time with your loved ones. I’ve taken a much needed moment this holiday to take a step back and think about all GFLF has to be thankful for. I owe so much to my clients, friends, and family who have helped make this year a successful one.

Here are just a few of the things GFLF has to be exceedingly grateful for:

To get to work with amazing clients and talented professional advisors.

Being entrusted with drafting and executing estate plans for Iowans, enabling them to pursue their estate planning goals, achieve peace of mind, and set a plan in place for the future for their loved ones.

Getting to work toward maximizing charitable giving in Iowa in our respective, wonderful communities.

But, really, this is a short list—the tip of the turkey, if you will—of what GFLF is perpetually thankful for.

With the cold weather upon us, there are few things more appealing than curling up with a warm beverage and an engaging book. I find the winter is a time to settle in and turn inward. It’s a season of consideration of how to better ourselves both personally and professionally.

This is why this month I’m adding Holding the Gavel: What Nonprofit Leaders Need to Knowby Nanette Fridman to the Gordon Fischer Book Club shelf. For anyone who currently or is thinking about serving on a nonprofit board, this book is like a guidebook on what to expect and how to be a successful, contributive member of the board. The book contains insider stories from people who have experience leading boards and valuable information on what good governance looks like.

Some of these sorts of books can get dreadfully boring or are too general to be applicable, but this book is both helpful and specific on topics ranging from how best to conduct due diligence to managing difficult board members.

When it comes to passing on and developing a board (and the organization it serves) and leaving it better than you found it, this roadmap of a nonfiction book is worth your time.

https://www.gordonfischerlawfirm.com/wp-content/uploads/2019/11/Screen-Shot-2019-11-24-at-9.14.43-PM.png6831038Gordon Fischerhttps://www.gordonfischerlawfirm.com/wp-content/uploads/2017/05/GFLF-logo-300x141.pngGordon Fischer2019-11-24 21:17:402020-05-18 11:28:41Pick up the November Book Club Title: Holding the Gavel

Based on every statistic I’ve seen, the majority of Americans don’t want anything to do with estate planning or the perceived headaches that come with it. However, making excuses to avoid investing in a valuable legal set of documents (that comes with numerous benefits) will do nothing to cement your legacy and intent for transfer of assets.

Here are some of the excuses I’ve heard from people about why they don’t have an estate plan:

“I don’t have any assets, and just a whole bunch of debt.”

“Getting a will made for myself is too expensive and time consuming.”

“If I talk too much about it, I might jinx myself.”

Yet, everyone over 18-years old, regardless of age, debts, assets, and marital status should have an estate plan in place. (Here are the six “must have” estate planning documents you can focus on initially.) In the beginning it may feel uncomfortable talking about the details of your estate plan—that’s normal. But, there is deep and lasting peace of mind in knowing that there is a plan in place in the event of your incapacitation or untimely death, which far outweighs any discomfort.

So, cast off all excuses by embracing the benefits of having a strong estate plan in place. The benefits include, but are certainly not limited to, peace of mind, financial security for your family, established guardianships for your children, reducing taxes, fees, and costs, and saving your family and friends untold time, trouble, and heartbreak.

https://www.gordonfischerlawfirm.com/wp-content/uploads/2018/11/Screen-Shot-2019-05-10-at-11.31.43-PM.png6511021Gordon Fischerhttps://www.gordonfischerlawfirm.com/wp-content/uploads/2017/05/GFLF-logo-300x141.pngGordon Fischer2019-11-21 09:10:572020-05-18 11:28:42Common Estate Planning Excuses and How to Avoid Them

Who – what age group – needs to be most concerned with estate planning? Ask Iowans this question, and I’ll bet most would conjure up the image of a retiree, who just spent 50+ years working hard to acquire significant assets.

But imagine, say, a young, married couple. They both have good jobs, live in a nice starter home, and have one or two toddlers.

This young couple tries to put away a little bit of money for savings, and in a college fund, and for retirement. Why should they worry about estate planning?

The truth is, this young couple should be just as concerned–arguably, even more concerned–with estate planning as the retiree. Here are four reasons why:

Choosing guardians for minor children. In an estate plan, you can choose the guardians of children. If you should become incapacitated, or even die, without any estate plan, an Iowa court would have no choice but to appoint a guardian for your children – but it may not be who you wanted or who you would have chosen. Better to make this choice with plenty of time to consider and make a careful, well-reasoned choice.

Save on fees, court costs, and taxes. A good estate plan can save you and your estate money on fees, court costs, and taxes – perhaps even achieve substantial savings. These savings can be even more critically important for a smaller estate – more likely when you’re younger – than for larger estate, more likely as you grow older. Often, young folks actually have the greatest need to save money to pass along the most they possibly can to family and loved ones.

Help favorite charities. Young people often are passionate about one or more causes. Having an estate plan means that you can put into place much needed help for your favorite charities.

Life is uncertain. It may be awkward to talk about, but life isn’t guaranteed for any of us, young or old. There’s an old saying in estate planning circles that goes, “people don’t always die when they are supposed to.” Wives usually outlive their husbands, parents usually outlive their children, and so on, but not always. It is best to be prepared for anything/everything.

https://www.gordonfischerlawfirm.com/wp-content/uploads/2017/05/sweet-ice-cream-photography-250621.jpg37975696Gordon Fischerhttps://www.gordonfischerlawfirm.com/wp-content/uploads/2017/05/GFLF-logo-300x141.pngGordon Fischer2019-11-20 19:49:552020-05-18 11:28:42Young Couples Should be the Most Concerned with Estate Planning

Giving Tuesday is held the Tuesday after Thanksgiving (December 3 this year) and is an important day for nonprofits to reach out to current and potential donors. Scroll through your social media feeds with the hashtag #givingtuesday and it seems like every organization, from big to small, is running digital marketing campaigns related to the day. Unlike Black Friday’s lines outside of stores in the middle of the night, #GivingTuesday’s activity is largely social media based. For nonprofits, all of this online activity is typically directed to online giving portals.

These online giving pages facilitate easy charitable giving, but before you send inspired donors to your giving portal, it’s wise to ensure your organization is compliant with associated legal issues. Whether you have created your own donation platform or are using a third-party platform embedded on your site, make sure to follow these legal tips:

Donation Receipt

It’s important to offer a donation receipt to your donors, so they make take the charitable contribution deduction on 2018 taxes if they choose so. A proper receipt—whether in a generated pdf, email, mailed letter, or other printed/printable form—should state the donor’s name, date of the contribution, and amount given.

If the donation is greater than $250 a written statement should be obtained stating that the organization did not give any services or goods. If the charity does, in fact, give goods or services to the donor in return for a donation, the acknowledgment should describe what was given and provide an estimate of value of the goods or services.

If those goods and services provided are valued greater than $75, the written statement must also specify the amount of the donation that is tax-deductible. (This figure is the amount of money that exceeded the value of the goods or services exchanged by the charity.)

You want to make certain your communications (such as written acknowledgments and receipts) with donors meet all legal requirements, as just discussed. But that doesn’t mean you can’t also have some fun with these communications, or use them as an opportunity to stick out above the noise with creativity. Here are a couple of solid articles, from The Balance and CauseVox featuring ideas for upgrading your thank you’s to donors.

Online Charitable Solicitations

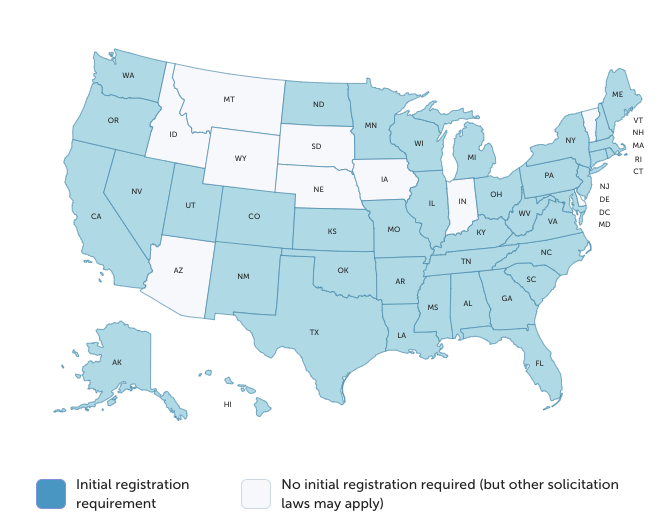

Fundraising activities fall under state law, and many states require charities (as well as individuals hired to assist the nonprofit with fundraising) to register with that state BEFORE any donations are solicited from residents of said state.

A charitable solicitation can be considered anything from a YouTube video with a call to action to donate, an e-newsletter sent to a subscriber list, to a simple Facebook post (and everything in between). Obviously, online giving has made figuring out which states your organization needs to register with complicated. Case in point, your organization may operate and be registered in Iowa, but if you have a “donate” button on your website, donations could come from residents of any state (or any country for that matter). Even the presence of a donation button could subject an organization to a registration requirement in some states, but won’t in other states. (Charitable solicitation registration is not currently required in Iowa.)

The main policy guidance for state regulators on this matter was published in 2001 by the National Association of State Charity Officials (NASCO), called the Charleston Principles. But, these provisions aren’t law, merely suggestive, so how should your charity deal with online donations? It’s far better for the organization to be safe rather than found noncompliant which can involve costly penalties.

Your charity could register (or file for an exemption) in all 41 states that require such registration, but that can be costly. The total fees to register your charity in all those states can range up to $5,000, (and that doesn’t even include professional fees you may need to incur, like paying lawyers or CPAs).

A second option is to register only with states that require registration and from which you would reasonably expect donations. For instance, if your nonprofit operates in Iowa, depending on your fundraising activities, it could be reasonable to expect donations from residents of neighboring states such as Minnesota. Or, if a significant percentage of subscribers to your e-newsletter is from Illinois, it’s smart to register there. With this option, it’s important to note that if you do receive a contribution from residents of another state that requires registration that triggers the need to register with that state.

Either way, it’s a good idea to look into the Unified Registration Statement (URS), a consolidated multi-state registration form. It’s also important to remember not only the initial registration but also registration renewals (complete with deadlines and late fees).

Crowdfunding Considerations

Crowdfunding is anticipated to be a $90-96 billion dollar industry by 2025, and there are more and more nonprofits utilizing it as a tool within the fundraising mix. If your charity is using a crowdfunding site (Kickstarter and Indiegogo are both popular platforms) the charitable solicitation registration requirements covered above apply. But, this is also a good subject to broach the topic of fraud and misrepresentation because crowdfunding has opened the door to more people being involved. Charitable organizations are prohibited from engaging in fraud, using deceptive practices that are likely to create confusion, and misrepresenting the nature, purpose, or beneficiary of the charitable solicitation. This one’s a biggie because committing fraud or misrepresentation could mean a lengthy and expensive litigation process.

To avoid this risk it’s wise to have a vetted gift acceptance policy with clear guidelines regarding crowdfunding. Organizations should keep an eagle eye on fraudulent crowdfunding campaigns that may use the nonprofit as a beneficiary, but fail to ever actually donate funds. Yet, if dedicated volunteers and donors do want to crowdfund for you, that’s fantastic. The organization just needs to keep a close watch on the campaign’s operation and offer crystal clear guidance on what campaigning on behalf of the charity is acceptable and what is not.

#GivingTuesday is coming up quick (where did the year go?!), so now’s the time to double check any potential issues for noncompliance that could occur. If you have any questions with regard to your online donation compliance I would love to offer a free one-hour consultation. Contact me via email or on my cell phone (515-371-6077). Best of luck with your #GivingTuesday campaigns!

When you create an estate plan one of the key benefits is that you’re dictating how you want your executor to distribute your assets when you pass away. An estate planning-related question I’ve gotten over the years is: “What about the house? Doesn’t my spouse just get the house straight away?” It’s true, many people do co-own real property (like a house) with their spouse. But, different types of concurrent estates (meaning co-ownership by two or more people) afford different rights to said co-owners.

So, the short answer to that commonly asked question about the house is: it depends.

Tenancy by Entirety

One type of co-ownership is called tenancy by entirety. This type exists only between spouses, and they hold the property (like a house) as one legal entity. If one spouse passes away, the surviving spouse takes the whole–becomes the sole owner–of the property.

This means the property would pass outside of probate, making for a simpler answer to the aforementioned “what about our house?” question. So, if something different was written in the deceased spouse’s will, this tenancy by entirety situation “wins” out. The same goes for if the spouse died intestate (without a will) and there’s no messing with which of the heirs-at-law gets what.

Another benefit is that the property is usually exempt from one spouse’s individual debts and liabilities. This means that a creditor couldn’t seize the property from the innocent spouse who is not legally responsible for the other spouse’s sole debts.

However, while this “special” concurrent estate come with the benefit of right of survivorship, there are certain limitations that come with it as well.

Spouses can choose to sever, mortgage, transfer, or sell the tenancy by the entirety, but neither can do so acting alone; both have to be in agreement.

It should also be noted that divorce terminates the tenancy by entirety.

Not in Iowa

Iowa does NOT recognize tenancy by entirety, but these 26 other states do. So, if you’re sharing this info with loved ones or if you co-own property in one of those states, you’ll want to speak with an experienced estate planner about how this type of concurrent estate fits in with your estate planning goals.

If this post wasn’t exciting enough for you and you want to learn even more about concurrent estates, you’re in luck! We’ll talk about tenancy in common and joint tenancy in the next couple posts.

Want to make certain your assets, including big ones like land or a house, pass how and to whom you choose? Schedule a free consult at your convenience and get started on my free, no-obligation estate plan questionnaire.

https://www.gordonfischerlawfirm.com/wp-content/uploads/2018/11/Screen-Shot-2018-11-26-at-10.38.22-PM.png6771100Gordon Fischerhttps://www.gordonfischerlawfirm.com/wp-content/uploads/2017/05/GFLF-logo-300x141.pngGordon Fischer2019-11-14 22:43:322020-05-18 11:28:42Legal Phrase of the Day: Tenancy by Entirety

If your child went to college this year you likely helped them acquire apartment/dorm essentials, review their class schedule, and file all the necessary paperwork for enrollment, student loans, financial aid, and the like. Give yourself a pat on the back; as a parent you should feel great that the small human you raised is beginning to charter the course for a successful, fulfilling life!

However, there are likely two important documents you (and your college student) didn’t have on the college prep list: power of attorney for healthcare and financial power of attorney.

I encourage every Iowan to have these essential documents a part of their quality estate plan. However, college students are in a unique position since many don’t yet have the need for a full estate plan if they don’t have children, pets, substantial financial assets, real estate, at the time they head off for their undergraduate education. But, even if a college student doesn’t have a need for an entire estate plan, they still need these power of attorney documents. Let’s review both.

Power of Attorney for Health Care

Apower of attorney for health care designates someone to handle your health care decisions for you if you are deemed unable to make those decisions for yourself. Your agent will be able to make decisions for you based on the information you provided in your health care POA. Equally important, your agent will be access your medical records, communicate with your health care providers, and so on.

Keep in mind that power of attorney for healthcare isn’t just about end-of-life decisions—it can cover any medical situation. So, in a worst case scenario, if your (adult) child were to have some sort of debilitating accident and were deemed by a medical professional unable to make health care decisions for themselves, then a trusted adult, like you (the parent), named as their health care representative could make such decisions in the best interest of their physical health. A similar situation could occur if your student were to have a mental health emergency. If deemed temporarily incapacitated by a doctor, health care power of attorney could allow you to commit them for the evaluation and treatment needed.

Thepower of attorney for finances is similar to the power of attorney for health care; your designated agent has the power to make decisions and act on your behalf when it comes to your finances. This gives the selected agent the authority to pay bills, settle debts, sell property, or anything else that needs to be done if you become incapacitated and unable to do this yourself.

While college students may not have many financial assets, their bank accounts, credit cards, and apartment leases in their name should all be taken into consideration and accounted for. Additionally, a financial power of attorney can cover digital assets including online accounts for their school, banking, email, and social media, among others. Without passing along the necessary digital information and instructions to digital accounts, parents if they’re the authorized representative, can face major headaches on issues such paying bills, accessing bank records, shutting down social media profiles, and the like she says.

Having power of attorney documents in place also prevents someone, like you as a parent, from having to go to court to get permission to act as the student’s proxy. Avoiding court at all costs is a wise plan as it’s both time consuming and expensive.

Does State Residency Matter?

A power of attorney that’s validly executed in the state in which an individual has full-time residency is usually honored across the U.S. But, what if your child is enrolled at a school out-of-state? Not a problem. Simply have your in-state attorney contact a recommended attorney in the state where the school is located to confirm the power of attorney document would be valid in that state and if not, recommend provisions to ensure it would be.

Why Now?

When your child is a minor (under age 18) you need certain legal documents such as nomination of guardianship. Once your child turns 18 (AKA becomes a legal adult) they are no longer under your immediate care as their guardian you as their parent are no longer responsible for making their healthcare decisions. Yet, all of us need someone we trust to make decisions in our best interest, which is why adults (even college students and young professionals) need power of attorney documents established.

How to get Started? Have a conversation.

As a parent you cannot force your college student to sign a power of attorney, but you may be one of the best people to discuss the topic. While a topic that includes debilitating injuries and the prospect of death is not a pleasant one for anyone involved, it’s nonetheless important. As a trusted adult you can explain how these documents could make a vital difference in some health and financial related situations. A good place to start in the conversation is explain what the documents are and how they can be used to execute their personal wishes.

https://www.gordonfischerlawfirm.com/wp-content/uploads/2017/09/muhammad-rizwan-270301.jpg32644928Gordon Fischerhttps://www.gordonfischerlawfirm.com/wp-content/uploads/2017/05/GFLF-logo-300x141.pngGordon Fischer2019-11-13 07:24:352020-05-18 11:28:42First in Class: Importance of Power of Attorney for College Students

“True heroism is remarkably sober, very undramatic. It is not the urge to surpass all others at whatever cost, but the urge to serve others at whatever cost.” -Arthur Ashe

On Veterans Day and every day, I want to say a heartfelt thanks for our veterans’ sacrifice and service. I work with many veterans on estate planning and in nonprofit-related work, and it’s always an honor. There are not enough “thank you’s” in the world to express my gratitude for what they have done for our country.

As a veteran your story is important. Your legacy is important. To preserve that legacy of strength and service, you need an estate plan to ensure your property and assets are distributed to your loved ones and favorite charities in accordance with your wishes.

So, in an attempt to express my gratitude I would like to offer 25% off the cost of an estate plan package to all Iowan active duty or retired service members. The discount will be honored through 11/30/2019. Contact me via email or by phone (515-371-6077) to discuss your estate planning needs.

What does an Estate Plan Include?

There are six documents that should be part of most everyone’s estate plan.

Because I want every Iowan to have an up-to-date estate plan I’m very transparent with the cost of an estate plan that takes into full consideration YOUR situation. (This is why you need an experienced estate planner to draft your documents.) Speaking very generally, an estate plan from my Firm usually costs a single person about $790, and a family about $990. So, with this Veterans Day discount, that’s a saving of about $197.50 for singles to $247.50 for a family.

I write about my process at length, but it’s just five steps! Seriously, it’s not that painful. My clients report back to me that they have such relief and peace of mind when it’s completed.

Contact

If you’ve been making excuses or have an extremely outdated estate plan now’s the time to check it off your list (and get a discount while doing so!).

The “Veterans Day discount” is only applicable for estate plans created by active or retired veterans (and their spouses). Availability of the discount ends after November 30, 2019 at which point the prospective client must have contacted Gordon Fischer Law Firm and indicated an intention to make an estate plan.

Veterans Day discount merely relates to pricing and in no way creates an attorney-client relationship, nor any other kind of professional relationship. The Veterans Day discount does not create a contract or agreement of any kind.

Gordon Fischer Law Firm, P.C. retains full and total discretion as to who it chooses to serve as clients and why. Gordon Fischer Law Firm, P.C. retains the right to refuse service to anyone it so chooses.

The Veterans Day discount may not apply to individuals or families with a high net worth of around/more than a million-plus dollars. (You still need an estate plan, very much so, but it necessarily needs to be more “complex” to adequately account for all assets.).

https://www.gordonfischerlawfirm.com/wp-content/uploads/2017/11/aaron-burden-97663.jpg30534479Gordon Fischerhttps://www.gordonfischerlawfirm.com/wp-content/uploads/2017/05/GFLF-logo-300x141.pngGordon Fischer2019-11-11 10:47:002020-05-18 11:28:42Thank You for Your Service: Veterans Day Estate Plan Discount

With its feast of turkey, stuffing, and mashed potatoes, Thanksgiving is the obvious holiday to look forward to in November. But the overall focus of Thanksgiving—the concepts of giving, sharing, practicing gratitude—is something you can cultivate for the entire month of November, especially on the lesser-known “holidays” of National Philanthropy Day and Giving Tuesday(technically in December this year).

National Philanthropy Day

On November 15 plan to celebrate National Philanthropy Day (NPD) with a donation of time or funding to a cause that’s near and dear to your heart. No matter how much you’re able to give, the point of this day to recognize that charitable donors and volunteers make a significant difference and impact. As the Association of Fundraising Professionals puts it:

“NPD is a celebration of philanthropy—giving, volunteering and charitable engagement—that highlights the accomplishments, large and small, that philanthropy—and all those involved in the philanthropic process—makes to our society and our world.”

A man by the name of Douglas Freeman conceptualized and organized the initial (unofficial) National Philanthropy Day in the early 1980s. Then in 1986, President Ronald Reagan designated NPD as an official day. NPD is also a key event a part of a grassroots movement that intends to raise awareness and interest for the importance of effective philanthropy.

Giving Tuesday

Popular on and spurred forward through social media, Giving Tuesday is often found with an accompanying hashtag (#GivingTuesday). Billed as a “global giving movement” Giving Tuesday is the Tuesday after Thanksgiving and after the shopping sprees of Black Friday and Cyber Monday. Held on December 3 this year, it’s seen as the sort of kickoff to end-of-year giving and it’s encouraged you donate your time, monetary donation, or even just your voice and ideas to a charity/cause that you care for.

With giving top of mind in November, maybe you have an idea for how you would like to support the important charities you care about but are unsure of how to go about making certain donations. For instance, did you know you can give to charity through your estate plan? How about the immense benefits of the retained life estate? How does giving fit in with your retirement benefit plan? I’m happy to help. Email me at gordon@gordonfischerlawfirm.com or drop me a line at 515-371-6077.